Phoenix Days on Market Surges 55% Year-Over-Year: April 2026 Analysis

Phoenix DOM Hits 82 Days — the Largest Year-Over-Year Jump Since the Pandemic Correction

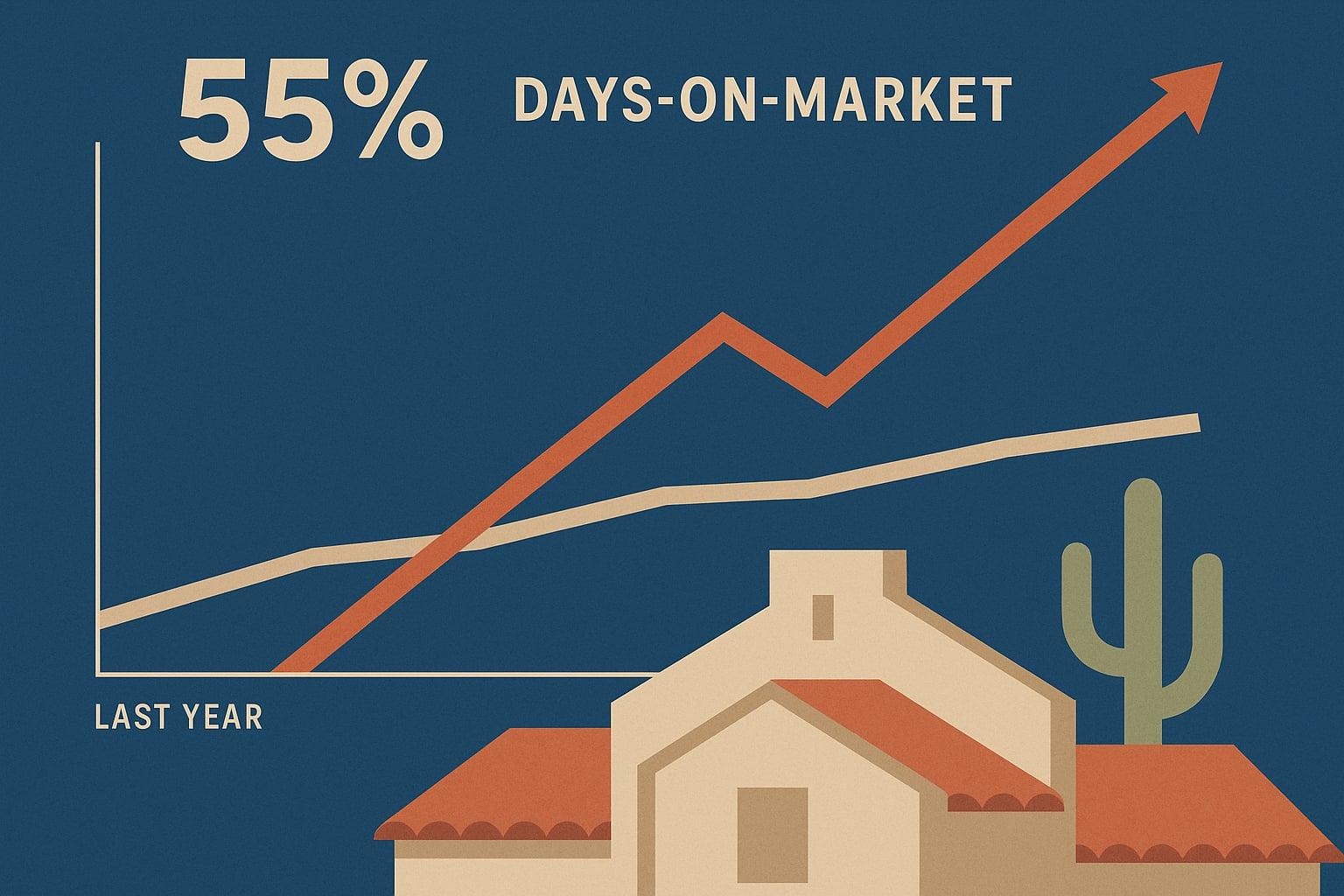

Phoenix properties averaged 82 days on market in April 2026, up from 53 days in April 2025, per Movoto's monthly market trends data. That 55% YoY acceleration is not a seasonal blip. It represents the steepest DOM expansion in the metro since inventory first began climbing off pandemic-era lows, and it is the clearest signal yet that negotiating leverage has decisively shifted to buyers.

A methodology note matters here. Movoto's DOM figure aggregates city-of-Phoenix listings and reflects the full listing-to-close cycle. ARMLS data for the broader Phoenix-Mesa-Chandler MSA, by comparison, logged a median DOM of 55 days in March 2026, per phoenixhomes.com — a difference explained by geography and how days are counted at contract versus close. Both series are moving in the same direction. The magnitude of the Movoto figure captures how long sellers inside city limits are actually waiting for a signed contract, which is the more operationally relevant number for anyone negotiating today.

The active listing count at the city level stood at 8,027, with 541 new listings added in April, per Movoto. Zooming out to the MSA, ARMLS data showed months of supply compressing from 4.42 to 3.34 between February and March 2026 as the spring buying season activated — a 24% single-month drop, per the ARMLS STAT Report. Supply at 3.34 months sits in seller-leaning territory by the conventional threshold: real estate professionals generally define under 3 months as a seller's market, 4 to 6 months as balanced, and over 6 months as a formal buyer's market.

Phoenix has not yet crossed the 6-month threshold. But the trajectory of the DOM series tells the more relevant story for investors.

The Sticky Seller Problem: $475K Ask, $460K Close

The median list price in April 2026 held at $475,000, per Movoto, essentially flat against prior months. Sellers are not cutting asking prices to reflect the demand signal that DOM is broadcasting. That stickiness has a name: anchoring to a purchase price or a neighborhood comp from 2022 or 2023, when the Phoenix market was running at peak.

The ask-to-close gap tells the real story. Redfin's March 2026 data puts the Phoenix median sale price at $460,000, a 5.2% YoY decline. Against Movoto's April list price of $475,000, the implied discount-to-list is running at roughly $15,000 per transaction at the median, a gap that widens further once concessions (rate buydowns, closing cost credits, repair allowances) are factored in. Houzeo's March 2026 analysis found the sale-to-list price ratio running below 100%, with a significant share of Phoenix homes carrying at least one price reduction.

Zillow's parallel valuation model places the average Phoenix home value at approximately $410,000, down over the prior 12 months. The divergence between valuation models is itself informative: it reflects a market where the composition of closed sales, skewed toward move-in-ready or well-located product, is supporting the median even as the broader value distribution drifts lower.

Tina Tamboer, senior housing analyst with the Cromford Report, drew the distinction that matters most for investors: "When we say it's a buyer's market, I don't want people to freak out. It's not the kind of buyer's market we saw in 2008."

Buyer Leverage Is Concentrated in Suburban and Entry-Level Segments

The aggregate Phoenix DOM figure masks an intra-metro split worth tracking. Redfin's neighborhood-level March 2026 data shows Downtown Phoenix median sale prices up 31.6% YoY to $520,000, with days on market compressing from 147 to 65 days. Walkable urban core inventory is absorbing demand. The pressure is concentrated in suburban and entry-level segments, where supply has accumulated fastest and where buyer hesitation, driven partly by 30-year fixed rates running in the 6.45%–6.55% range per phoenixhomes.com's early April 2026 reading, is most acute.

The stale-listing dynamic is not new. Redfin data cited by Axios found that more than 47% of Phoenix home listings in April 2025 had been on the market for 60 days or longer without going under contract. That figure predates the April 2026 DOM surge and suggests the inventory overhang in suburban price bands has been building for more than a year.

For investors underwriting acquisitions in that suburban band, the current DOM expansion translates directly into negotiating surface. Extended time on market erodes seller certainty, increases the carrying cost of an unsold listing, and raises the probability that a seller will accept contingencies they would have rejected in 2022. Inspection contingencies, appraisal gaps, and rate-buydown seller credits are all back on the table in segments where DOM is running well above the metro median.

The Supply Trajectory Into Summer 2026

Phoenix metro inventory grew 19.2% YoY through late 2025, reaching approximately a 4.4-month supply per Phoenix REALTORS data reported by AZ Big Media — the highest balance in nearly a decade. The spring 2026 selling season compressed that figure temporarily, as ARMLS data confirmed months of supply dropped to 3.34 in March. Whether the seasonal demand pulse holds through summer is the open question.

Phoenix summers historically soften demand as heat discourages touring activity. If new listings continue entering at the pace seen in early 2026 while buyer absorption moderates — the pattern seen from May through September in most recent years — months of supply will drift back toward the 4 to 5 range by August. At 6 months, by the standard industry definition, the market tips formally into buyer's territory. The current trajectory does not guarantee that outcome, but it does not rule it out.

The investor framing is straightforward: the window of maximum seller concession availability typically precedes a formal buyer's market designation by several months, as sellers capitulate on contingencies and credits before cutting ask prices. Phoenix appears to be in that window now. The question is how long the spring absorption surge sustains the supply compression before summer seasonality reasserts.

For deeper context on how Phoenix's price trajectory fits the broader Sun Belt correction, see the AEI Sun Belt Home Price Decline Analysis and the companion piece on Phoenix's median sale price decline through March 2026.

Subscribe to the SunBeltPulse weekly data brief for updated Phoenix months-of-supply and DOM readings as the summer selling season develops.

This article was researched and drafted with AI assistance, fact-checked, and reviewed by an editor before publication — see our Editorial Standards. It is general information about real estate markets, not financial, investment, legal, or real estate advice; consult a licensed professional before acting. See our full disclosure.

More market analysis

Phoenix Is Still Growing: Why Domestic Migration Keeps Flowing Into the Valley While the Rest of the Sun Belt Stalls

5 min read

AEI Projects National Home Prices Turn Negative in April 2026 — What It Means for Phoenix, Austin, Tampa, Nashville, and Charlotte

7 min read

Phoenix Is Finally a Buyer's Market — Here's What the Data Shows

6 min read

Beyond the calculator: see our full relocation toolkit — movers, agents, insurance, and city-test rentals.